Visa: The Security I Like Best

If you were to design the perfect business, it would look something like the IRS. A business that takes a portion of all transactions, benefiting from all new and existing economic activity, and doing so with little overhead. In 2021, the IRS collected $4.1T in gross taxes on $13.7B of expenditures. 99.7% margin, put that in your DCF!

The IRS is too valuable to actually calculate. And unfortunately, we can’t directly own a piece of a government agency. But we can own the most IRS-like business, Visa.

Industry:

Visa and MasterCard collectively processed $19.8T of payments volume in the last twelve months. That’s ~20% of global GDP, up from around 14% in 2017, and it could get much higher.

Global payments volume is larger than global GDP. Multiple transactions are often needed to create one GDP item. Payments volume is a persistent, unstoppable trend that will always be growing if the economy is growing. Even inflation won’t stop Visa.

“net-net, historically inflation has been positive for us.” -Visa CEO Al Kelly

When economies grow, new units of production are created, decreasing the value of existing units. This works to the benefit of the card networks who maintain their share of consumer spending if they maintain take rates, just like the IRS can with the overall economy. Of course, if near term inflation is high enough to crater consumer spending and cause instability, it becomes a negative.

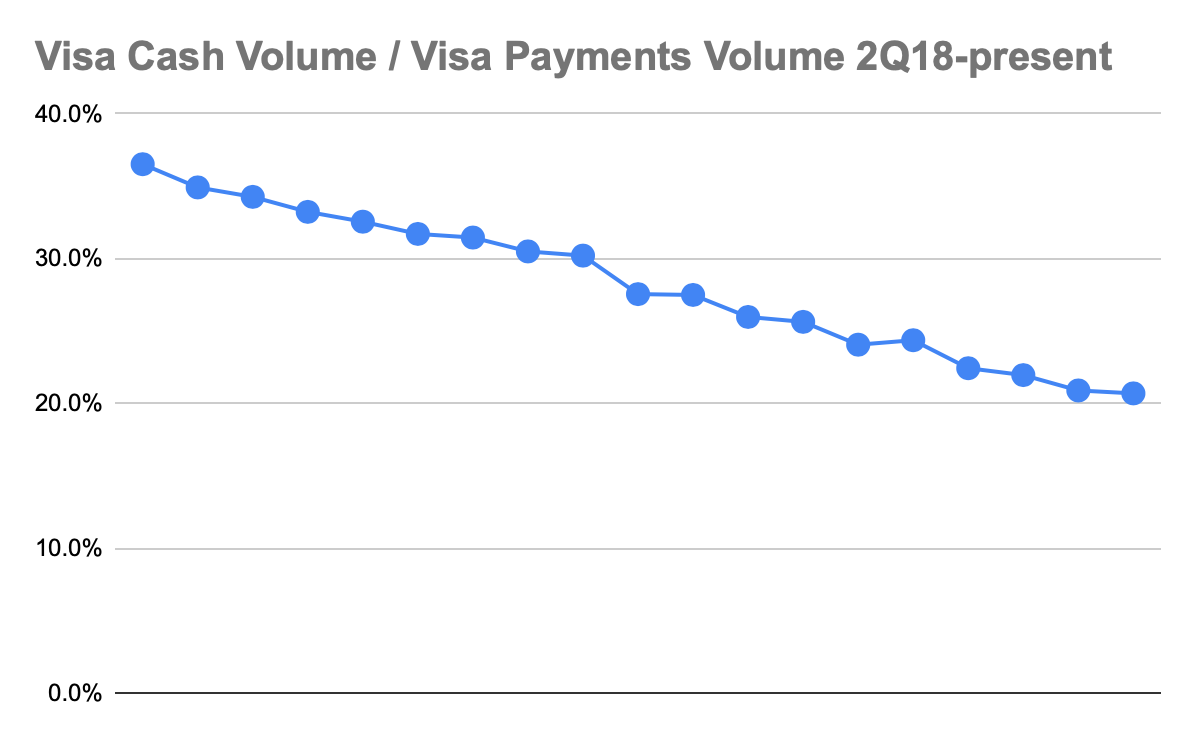

Along with the economy growing, the economy is modernizing. In certain places around the world, cash is still a dominant method of payment. Visa reports “cash volume” in its quarterly operational data that consists of cash access transactions, balance access transactions, balance transfers, and convenience checks. This isn’t perfect, but comparing this number to Visa’s payment volumes is a decent representation of the cash to cashless transition:

Eventually, all industries mature and growth slows. 100 years ago, automobiles were the most exciting area of growth. Today, not so much. Investing for the long run requires us to own businesses where we have a solid idea of where growth can come from 10 or 20 years from now. You will most certainly be spending money on products and services that don’t exist yet using Visa credentials.

I’m not the first person to figure out payments are an incredible industry. Every expense software and e-commerce marketplace wants to integrate payments and charge customers per transaction. But these efforts are often a different way of charging customers for the same service. They won’t benefit from the same industry level tailwinds as Visa.

Competitive Position:

Visa and MasterCard are open networks. The open networks allow banks to communicate when purchases are made. American Express and Discover are closed networks. Closed networks are FDIC insured banks that issue their own lines of credit. They control the whole process, so they get the issuer fee and the network fee, but their total addressable market is confined by customer acquisition.

Issuing is a highly competitive, highly fragmented, commodity industry. But it’s an important commodity. And thousands of issuers have just two networks to run on.

Despite the regulatory pushback from Senator Richard Durbin over the past decade, the card networks are stronger than ever. The original Durbin Amendment was passed as part of Dodd Frank in 2010 and allowed the Federal Reserve to set interchange fees and routing requirements for debit cards. Durbin’s new proposal wants to bring similar regulation to credit cards:

“For years I have worked to bring fairness and competition to credit and debit card swipe fees. These swipe fees inflate the prices that consumers pay for groceries and gas...That’s outrageous, and we’re going to find out which banks and card networks are profiting off of these surcharges...With these amendments, we can bring real competition to credit card networks to help reduce swipe fees and hold down costs for Main Street merchants and their customers; and bring transparency to the shameful surcharge fees...” -Senator Durbin

Despite the saber rattling from Durbin, Visa’s competitive position as the network in between the banks was unknowingly solidified with Glass-Steagall. Visa isn’t even the prime culprit for high swipe fees.

The chart below shows the flow of each transaction, in percentage terms, 87% of fees go to issuers, 8% goes to the acquirer, and Visa collects 5%:

Much of the fee issuers receive are returned to consumers through rewards programs. The argument can be made this is regressive, wealthier consumers are more likely to pay on time and enjoy the benefits of credit cards as opposed to getting behind and paying huge interest on debts.

But given how Visa’s business is nearly a 50/50 split between credit and debit, consumers are eager to use Visa payments regardless if there’s issuer rewards.

The networks provide low cost, easy to use access to economic participation. By the time Visa’s fees are added up, the take rate is a meager 0.25% of total payment volume. Average processing fees are anywhere from 1.5-3.5%, meaning Visa’s take is very small for the value provided. It’s easier to argue why the card networks take rate is too low.

Most experts believe Visa will simply pass fees off to merchants if the Durbin Amendment was extended to credit:

“(the networks) would do what they’ve done with debit, they would increase their ‘fixed’ network access fee. Visa introduced a big new fee when the Durbin Amendment took effect. Every merchant that accepts Visa pays a fixed fee per month, it’s tied to number of merchant locations and payment volume, but it’s not paid on a transaction by transaction basis. The idea is every merchant thinks they have to accept Visa, and that’s by and large true. The DOJ took a look at the time and didn’t raise any antitrust concerns against Visa.” - Anonymous Tegus Expert

With 4B credentials around the world, any merchant not accepting Visa would have a material impact on business. This gives Visa enormous pricing power that management needs to intelligently flex over time. Amazon tried to stoke the fire by not accepting Visa in the UK, but quickly scrapped that plan.

Reinvestment Opportunities:

Visa’s revenue has compounded at over 15% for the past 20 years. Visa has a realistic chance at continuing to compound core revenue at a double digit rate. The driving factors of general payments volume growth, runway in the cash to cashless transition, and pricing power would help them get there.

In addition to Visa’s core consumer payments business, there’s opportunity in new flows and value added services. Visa has numerous bets here that investors must trust management’s discretion on. New flows are extremely small compared to Visa’s core thus far. Visa Direct is the largest segment of new flows and had just 5.9B transactions last fiscal year compared with 240.8B total payments transactions.

Other areas the card networks are venturing into are remittances and disbursements, commercial point of sale, virtual cards, and B2B accounts payable. Luckily for investors, these investments make no noticeable dent in Visa’s stellar financials.

Margins & Capital Allocation:

Visa has incredible margins and capital allocation.

“I worked at Visa. Visa bought my company. It's a very simple business to operate...They need probably 10 people to keep the lights on...And it's actually kind of remarkable, when was the last time they had an outage? All of these newfangled tech companies with amazing engineers, they seem to go down all the time…Visa and MasterCard do not go down. It's pretty remarkable that they've been able to pull that off.” -Alex Rampell

Visa’s gross profit per employee minus median compensation is over $1M. CapEx is less than 5% of revenue. This reflects in their free cash flow margins over 50%. There’s immense operating leverage in transaction growth.

Visa is extremely shareholder friendly. They have consumed about 10% of the shares outstanding over the past 5 years and pay a small dividend to entice yield seekers.

Other than Visa acquiring its former subsidiary Visa Europe for $23B in 2016, Visa spends very little on acquisition. Their $2B acquisition of Tink last fiscal year was the second largest in their history as a public company. There’s plenty of history suggesting Visa will continue to be responsible stewards of capital moving forward.

What’s Next:

Visa had a remarkably strong fiscal 2022. Inflation has appeared to be a tailwind for Visa as consumers spending has remained strong, even as mix has shifted.

“there's stability, the reality is we do know that there's some changes in consumer behavior going on, but they're still spending the same amount of money, and they're still paying in the same way, which are critical to us.” -Al Kelly

Visa trades at ~25x FCF on modest expectations for flattish FCF growth over the next year. This is a lower multiple than Visa typically trades at, but that’s expected given the overall level of economic uncertainty.

Near term uncertainty will be the biggest hurdle for Visa. Visa’s fundamentals are so strong it’s a hold and monitor. The current share price is good, and might be too low if FCF shows higher growth this fiscal year, or a bit too high if the slowdown persists.